Posted by – QPIN Insights

Executive Summary

The implementation of GST 2.0 in September 2025 represents a structural shift in the Indian indirect tax regime. With two revised slabs of 5% and 18% and the elimination of long-standing “magic price points” such as ₹5 and ₹10, FMCG companies must now re-examine their pricing architecture, portfolio design, and channel economics.

This is not a compliance adjustment-it is a strategic inflection point for the consumer products industry. The ability of leadership teams to adapt quickly will determine market share outcomes over the next decade.

Why the ₹5 and ₹10 Packs Were Strategic Assets

For more than two decades, low-unit packs (LUPs) priced at ₹5 and ₹10 have been a cornerstone of FMCG penetration and brand building. They enabled:

- Rural market access: Ensuring affordability for low-income households across India’s 600,000+ villages.

- Consumer trials: Reducing entry barriers for new customers and driving adoption of premium brands.

- Value perception anchoring: Fixing consumer expectations around “trust points” that shaped brand loyalty.

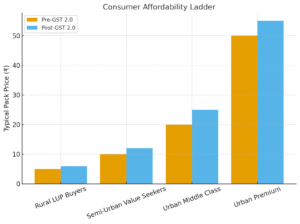

The GST 2.0 regime disrupts this equilibrium. A ₹5 pack of biscuits may now need to be priced at ₹6–₹7; a ₹10 shampoo sachet at ₹12. Such changes risk consumer resistance and substitution toward local or unbranded alternatives.

Early Market Signals

- Rural demand resilience: Rural markets have posted five consecutive quarters of consumption growth (NielsenIQ, 2025). However, this demand is highly price-elastic; consumers switch rapidly once affordability thresholds are breached.

- Industry pilots: Leading players such as HUL and ITC are reportedly testing ₹7 and ₹12 packs in semi-urban and rural clusters. Startups are adopting bundling strategies to maintain value perceptions.

- Retailer feedback: Kirana store owners highlight that if ₹5/₹10 packs disappear, unbranded substitutes will quickly capture value-conscious consumers.

Strategic Imperatives for FMCG Leaders

GST 2.0 forces a strategic realignment across multiple levers. CXOs must lead with an integrated response:

- Portfolio Re-engineering

- Introduce intermediate price points (₹6, ₹12, ₹15) to smooth the affordability ladder.

- Redesign grammage architecture to protect margins while addressing consumer psychology.

- Cost Transformation

- Localize sourcing and regionalize supply chains to mitigate logistics and tax-related cost pressures.

- Pursue value engineering in packaging, including lightweight laminates and recycled inputs.

- Channel Strategy

- Leverage quick commerce and e-commerce to push premium SKUs where consumers accept higher price points.

- Revise incentive structures for rural distributors to ensure non-₹5/₹10 SKUs gain traction.

- Consumer Communication

- Reframe pricing changes through messaging around “new pack, more value.”

- Use narratives on health, taste, or sustainability to justify premiumisation and build consumer acceptance.

The Long-Term Outlook

By 2030, nearly 40% of FMCG consumption in India is projected to be online (Redseer, 2025). At the same time, rural markets are expected to contribute nearly half of incremental FMCG volume growth.

The implication is clear:

- Urban consumers will drive premiumisation through digital channels.

- Rural consumers will remain the volume growth backbone, where affordability and accessibility must be defended.

Companies that realign pack architecture, reconfigure supply chains, and evolve consumer messaging will secure long-term competitive advantage. Those that fail to act decisively risk erosion of share to local insurgents and D2C challengers.

Advisory Note for CXOs

GST 2.0 is a business model reset, not a tax adjustment. Leadership teams should prioritise:

- Rapid scenario planning across categories and price points.

- Micro-market pilots to test affordability thresholds before national rollout.

- Cross-functional cost optimisation that balances innovation with efficiency.

- Strategic partnerships with independent consultants to access expertise in pricing architecture, consumer insights, and supply chain redesign.

Conclusion

The disruption of ₹5 and ₹10 packs marks the end of an era in Indian FMCG. The companies that succeed in the GST 2.0 landscape will be those that anticipate consumer behaviour shifts, innovate in pack-price architecture, and invest in agility at scale.

For CXOs, the question is not whether to adapt-it is how quickly and how decisively.